Financial needs arrive unexpectedly, and having access to fast, reliable credit can make an enormous difference in how confidently you navigate them. Onnilaina offers a streamlined way to apply for quick online consumer credit without the complexity, paperwork, and frustrating delays that traditional lending processes typically demand. The platform delivers speed, transparency, and genuine accessibility to individuals who need flexible financial solutions that fit their real lives. Furthermore, it removes the intimidation that many people associate with borrowing by creating a clear, straightforward process from application to approval. This article explains everything you need to know about how this lending solution works, who qualifies, and how to apply successfully.

Understanding Consumer Credit in the Digital Age

How Online Lending Has Transformed Borrowing

Traditional bank lending required physical visits, extensive documentation, long waiting periods, and often opaque decision-making processes. Consequently, millions of people found conventional borrowing unnecessarily stressful, time-consuming, and inaccessible during moments of genuine financial need. Furthermore, digital lending platforms emerged to address these pain points by leveraging technology to simplify and accelerate every step. Moreover, online consumer credit now reaches people who previously lacked convenient access to fair and transparent borrowing options. Additionally, automated assessment systems process applications far faster than human underwriters while maintaining rigorous and fair evaluation standards. Understanding this transformation helps explain why digital consumer credit solutions have attracted such significant and growing user adoption.

What Consumer Credit Actually Means

Consumer credit refers to money that individuals borrow for personal use rather than for business investment or commercial purposes. Therefore, common uses include covering unexpected expenses, consolidating existing debts, financing home improvements, or managing temporary cash flow gaps. Furthermore, consumer credit differs from mortgages and business loans in its typically shorter terms, faster processing, and more flexible qualifying criteria. Moreover, responsible consumer credit use helps individuals manage financial volatility without depleting savings or disrupting long-term financial plans. Additionally, understanding what consumer credit is and how it functions helps borrowers make informed decisions that serve their genuine financial interests. Approaching any borrowing decision with clear knowledge produces better outcomes than applying impulsively without understanding the commitment involved.

Why Speed Matters in Modern Financial Solutions

Financial emergencies rarely announce themselves in advance or wait politely while borrowers navigate slow institutional processes. Consequently, the speed at which a lending solution processes and approves applications carries enormous practical importance for real borrowers. Furthermore, quick credit access prevents small financial gaps from escalating into larger problems with more serious long-term consequences. Moreover, digital platforms that deliver same-day or next-day decisions genuinely change the financial resilience capacity of people who use them. Additionally, fast processing does not need to come at the expense of fairness, transparency, or responsible lending practice when platforms design their systems thoughtfully. Speed combined with integrity represents the genuine value proposition that the best digital consumer credit solutions deliver to their users.

What Makes Onnilaina Stand Out

A Fully Digital Application Process

The entire application process happens online, eliminating the need for branch visits, printed forms, or in-person appointments. Therefore, you can apply from anywhere with internet access using a smartphone, tablet, or computer at any convenient time. Furthermore, the digital interface guides you through each application step with clear instructions that prevent confusion or costly mistakes. Moreover, document submission happens electronically, removing the delays associated with physical mail or fax-based document transfer. Additionally, the fully digital nature of the process means that applications move through assessment stages faster than any paper-based alternative could manage. This complete digitization of the borrowing experience reflects a genuine commitment to serving modern users on their own terms.

Transparent Lending Terms From the Start

Many lending products bury important terms in dense legal language that most borrowers never read or fully understand. Consequently, this platform prioritizes complete transparency by presenting all relevant terms clearly before you make any commitment. Furthermore, interest rates, repayment schedules, total cost of borrowing, and fee structures all appear in plain language during the application. Moreover, comparison tools within the platform help you understand exactly what different loan amounts and terms will cost you. Additionally, no hidden fees emerge after approval — what you see during the application accurately reflects what you will actually repay. This commitment to upfront transparency builds the trust that makes borrowers feel genuinely confident rather than anxious about their credit decisions.

Flexible Credit Amounts and Repayment Terms

Different financial situations require different credit solutions, and flexibility in both amount and term matters enormously to real borrowers. Therefore, the platform offers a range of credit amounts that accommodate everything from minor unexpected expenses to more significant financial needs. Furthermore, repayment term options give borrowers meaningful control over how they structure their obligations relative to their income. Moreover, choosing a longer repayment term reduces monthly payment amounts while choosing shorter terms reduces total interest costs over time. Additionally, the platform’s interface makes it easy to compare different amount-and-term combinations to find the combination that best serves your specific situation. This genuine flexibility distinguishes thoughtful lending solutions from rigid products that force borrowers into ill-fitting structures.

Fast Decision and Funding Timeline

Waiting days or weeks for a credit decision defeats the purpose of seeking fast financial solutions during genuine need moments. Consequently, the platform processes applications rapidly and communicates decisions clearly without keeping borrowers in unnecessary suspense. Furthermore, approved applicants typically receive funds in their nominated bank accounts within one business day of completing the full process. Moreover, automated assessment technology evaluates applications continuously, meaning submissions made outside traditional business hours still receive prompt attention. Additionally, clear communication at every stage keeps borrowers informed about their application status without requiring them to make anxious follow-up inquiries. This rapid timeline from application to funded account represents one of the most practically important advantages this platform offers.

Who Can Apply for Onnilaina

Basic Eligibility Requirements

Understanding eligibility requirements before applying saves time and prevents unnecessary credit inquiries that temporarily affect credit scores. Therefore, applicants must meet specific baseline criteria that the platform communicates clearly and accessibly before the application begins. Furthermore, age requirements typically specify that applicants must have reached legal adulthood as defined by their country of residence. Moreover, applicants need a valid government-issued identification document that confirms identity and residency status unambiguously. Additionally, a bank account in the applicant’s name provides the necessary vehicle for both fund disbursement and repayment collection. Meeting these baseline requirements positions applicants to move through the full assessment process without encountering avoidable obstacles.

Income and Employment Considerations

Lenders need confidence that borrowers possess the financial capacity to meet repayment obligations without undue hardship. Consequently, demonstrating sufficient and reliable income represents a core component of any successful consumer credit application. Furthermore, employed applicants typically demonstrate income through recent payslips, employment contracts, or bank statements showing regular salary deposits. Moreover, self-employed applicants can demonstrate income through tax returns, business account statements, or accountant-verified income documentation. Additionally, some platforms consider multiple income sources including freelance work, rental income, and government benefits when assessing overall repayment capacity. Presenting your income situation honestly and completely gives the assessment system the accurate information it needs to make fair and appropriate decisions.

Credit History and Its Role

Credit history informs lenders about how applicants have managed previous borrowing obligations and financial commitments. Therefore, a positive credit history demonstrating timely repayments strengthens applications and may unlock more favorable interest rates. Furthermore, applicants with limited credit history should not automatically assume rejection, as the platform considers multiple assessment factors simultaneously. Moreover, some negative credit history items carry more weight than others, and recent positive financial behavior can meaningfully offset older negative records. Additionally, checking your credit report before applying helps you understand your starting position and address any errors that might unfairly disadvantage your application. Knowledge of your own credit position empowers you to approach the application process with realistic expectations and genuine confidence.

Residency and Documentation Requirements

Lenders operate within specific regulatory frameworks that establish who they can legally serve and what documentation they must collect. Consequently, applicants need to demonstrate residency in the geographic area the platform serves through appropriate supporting documentation. Furthermore, proof of address documents like recent utility bills, bank statements, or official correspondence establish residency effectively. Moreover, the platform specifies exactly which documents it accepts, eliminating guesswork about what you need to gather before applying. Additionally, ensuring that all submitted documents remain current and clearly legible prevents processing delays that extend the time before you receive a decision. Preparing all required documentation before beginning your application creates a smoother and faster experience from start to finish.

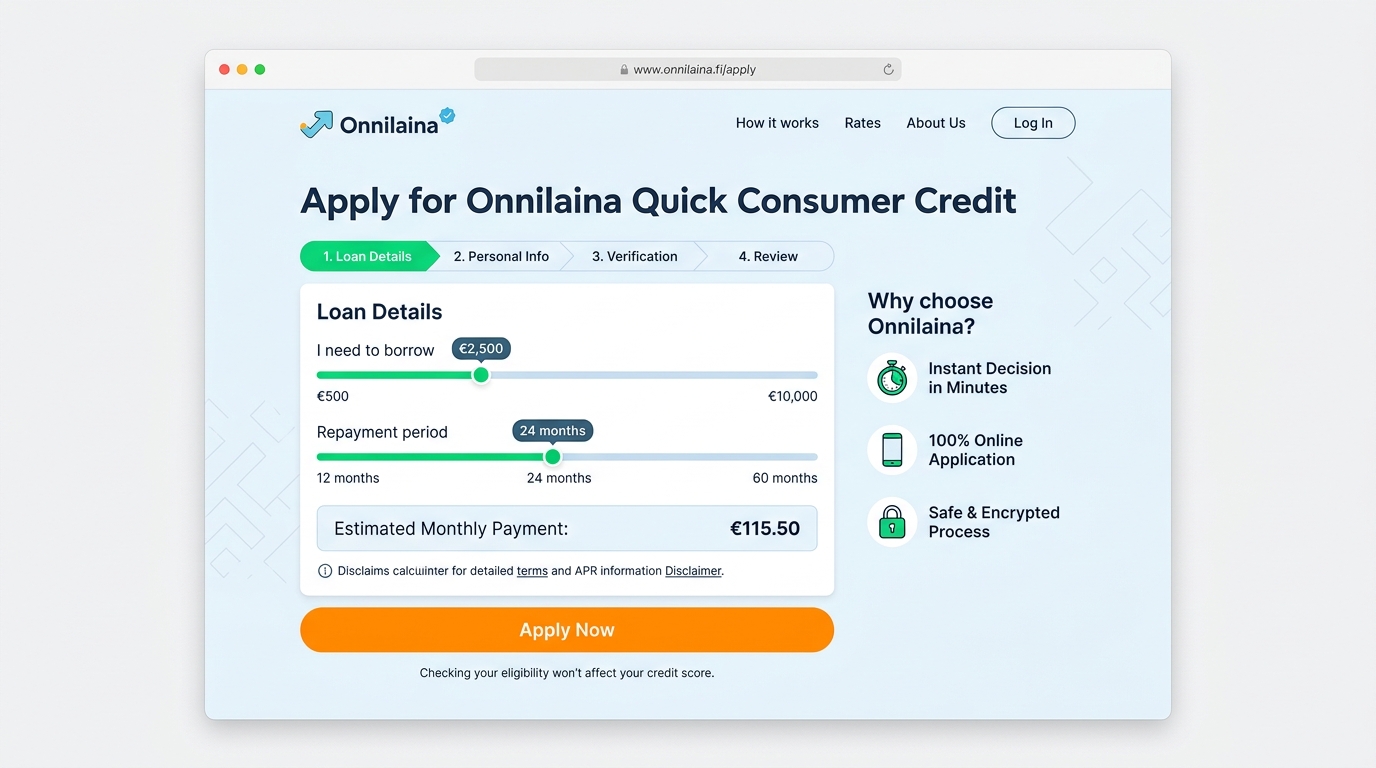

The Application Process Step by Step

Step One: Gather Your Information and Documents

Successful applications begin with preparation that ensures you have everything needed before starting the online form. Therefore, collect your identification documents, income evidence, bank account details, and proof of address before opening the application. Furthermore, knowing the exact amount you want to borrow and your preferred repayment term helps you move through the form decisively. Moreover, having your employment details, employer contact information, and monthly expense estimates ready prevents mid-application interruptions. Additionally, reviewing your recent bank statements gives you an accurate picture of your current financial position that the application will ask you to describe. This preparation investment typically takes fifteen to twenty minutes but prevents the frustration of stopping partway through an incomplete application.

Step Two: Complete the Online Application Form

The application form captures the essential information the platform needs to assess your eligibility and appropriate credit limit. Consequently, work through each section carefully and accurately rather than rushing to complete the form as quickly as possible. Furthermore, personal information sections require your full legal name, date of birth, address history, and contact details. Moreover, financial information sections ask about your employment status, monthly income, regular expenses, and existing financial commitments. Additionally, the loan selection section allows you to specify your desired credit amount and preferred repayment term before submission. Reviewing all entered information for accuracy before submitting prevents the delays that corrections and clarifications inevitably cause after submission.

Step Three: Submit Supporting Documentation

After completing the form, the platform typically requests supporting documents that verify the information you have provided. Therefore, upload clear, current, and complete versions of each requested document using the platform’s secure document submission system. Furthermore, identification documents should clearly show your full name, photograph, date of birth, and document number without obstruction. Moreover, income documents should cover a sufficient recent period to give the platform confidence in the consistency of your earnings. Additionally, bank statements should show your account number, your name, and recent transaction history that reflects your described financial position. Submitting complete and high-quality documentation in a single upload avoids the back-and-forth that incomplete submissions always generate.

Step Four: Wait for the Assessment Decision

Modern digital assessment systems evaluate applications far faster than traditional manual review processes ever could manage. Consequently, many applicants receive preliminary decisions within minutes of submitting complete applications with all required documentation. Furthermore, the platform communicates decision outcomes clearly through your registered email address and within the platform itself. Moreover, approved applicants receive a formal credit offer that specifies the approved amount, interest rate, repayment schedule, and total cost. Additionally, the offer period gives you time to review terms carefully before formally accepting the credit commitment. Taking time to read the offer document thoroughly before accepting ensures that you genuinely understand and agree with the terms you commit to.

Step Five: Accept the Offer and Receive Funds

Accepting a credit offer completes the formal borrowing process and initiates the fund transfer to your nominated account. Therefore, review the acceptance document carefully, confirm your bank account details, and complete the digital signing process. Furthermore, fund transfers typically process within one business day of acceptance, though some applicants see funds arrive more quickly. Moreover, the platform sends confirmation communications that specify the exact transfer timeline and provide reference information for your records. Additionally, your repayment schedule begins as specified in your credit agreement, so marking your first repayment date immediately prevents accidental missed payments. Organizing your repayment reminders from the very first day sets a positive pattern that makes timely repayment feel natural and manageable throughout your credit term.

Responsible Borrowing: What Every Applicant Should Know

Borrow Only What You Genuinely Need

The availability of credit creates temptation to borrow more than the situation actually requires, which creates unnecessary long-term cost. Consequently, calculating your actual financial need precisely before applying helps you request an amount that serves rather than burdens you. Furthermore, borrowing less than your maximum approval allows you to manage repayments more comfortably within your existing budget. Moreover, interest accumulates on the outstanding balance, which means larger amounts generate larger total costs across the full repayment term. Additionally, resisting the temptation to round up your borrowing to convenient numbers helps maintain the discipline that responsible credit use requires. Treating credit as a precise financial tool rather than a general financial buffer produces much better long-term outcomes for your financial health.

Understand the Total Cost of Borrowing

Interest rates describe the cost of borrowing as a percentage but can obscure the actual cash amount you will repay. Therefore, calculating the total repayment amount — principal plus all interest and fees — grounds your decision in concrete financial reality. Furthermore, comparison tools that show different scenarios side by side help you make genuinely informed decisions about amount and term. Moreover, understanding how repayment terms affect total costs allows you to make deliberate trade-offs between monthly affordability and overall expense. Additionally, asking yourself whether the purpose of the borrowing justifies the total cost it will generate helps maintain borrowing discipline over time. Responsible borrowing always begins with honest engagement with the full financial reality of the commitment you consider making.

Plan Your Repayments Before You Borrow

Agreeing to repayment obligations without a concrete plan for meeting them represents one of the most common and costly borrowing mistakes. Consequently, mapping your monthly income against your existing expenses before adding a new repayment obligation shows you the genuine affordability picture. Furthermore, identifying exactly which spending category will fund your monthly repayments creates a concrete and actionable plan rather than vague intention. Moreover, building a small buffer into your repayment planning protects you against minor income fluctuations that might otherwise create difficulty. Additionally, setting up automatic payment arrangements from your bank account eliminates the risk of missed payments due to simple forgetfulness. Planning repayments with this level of specificity transforms a borrowing intention into a genuinely executable financial commitment.

Know Your Rights as a Borrower

Consumer credit regulations protect borrowers from unfair practices and give them meaningful recourse when problems arise. Therefore, familiarizing yourself with the basic rights that apply to consumer credit agreements in your jurisdiction serves your genuine interests. Furthermore, the right to receive clear pre-contract information, cooling-off periods, and complaint resolution processes all exist to protect borrowers. Moreover, understanding that you can contact regulatory authorities if a lender violates your consumer rights gives you important protection knowledge. Additionally, reputable platforms like this one design their processes to comply fully with applicable consumer protection regulations as a matter of genuine principle. Knowing your rights empowers you to engage with any lending relationship from a position of informed confidence rather than vulnerability.

Managing Your Credit After Approval

Setting Up Successful Repayment Habits

Successful credit management begins the moment you receive funds rather than waiting until the first repayment falls due. Consequently, immediately scheduling your repayment dates in your calendar creates the awareness that prevents accidental missed payments. Furthermore, setting up automatic bank transfers for repayment amounts ensures that obligations meet themselves without requiring monthly active management. Moreover, keeping your bank account sufficiently funded around repayment dates prevents the fees and credit score damage that failed automatic payments generate. Additionally, treating your credit repayment as a non-negotiable fixed expense rather than a flexible cost maintains the repayment discipline that protects your financial reputation. These simple habits make credit management feel effortless rather than stressful throughout your repayment term.

Communicating Early if Difficulties Arise

Financial circumstances change unexpectedly, and borrowers who face genuine repayment difficulty sometimes make the mistake of staying silent. Therefore, contacting the platform proactively at the first sign of potential repayment difficulty produces far better outcomes than avoiding communication. Furthermore, lenders typically prefer working with borrowers to find manageable solutions rather than initiating formal collection processes unnecessarily. Moreover, early communication about genuine financial hardship often results in temporary arrangements that prevent credit record damage and escalating fees. Additionally, documenting all communications about repayment difficulties creates a clear record that protects your interests throughout any resolution process. Proactive, honest communication with lenders during financial difficulty represents one of the most practically important borrowing skills anyone can develop.

Final Thoughts

Accessing quick online consumer credit has never been more straightforward for people who approach the process with preparation and genuine financial awareness. Furthermore, this platform delivers the speed, transparency, and flexibility that modern borrowers need without sacrificing the responsible lending practices that protect everyone involved. Understanding the application process, eligibility requirements, and responsible borrowing principles positions you to use consumer credit as the genuinely useful financial tool it can be. Moreover, approaching borrowing with honesty about your needs, realistic assessment of your repayment capacity, and knowledge of your rights transforms credit from a source of anxiety into a source of genuine financial empowerment. As digital lending continues evolving through 2026, informed and prepared borrowers consistently achieve the best outcomes from every credit relationship they enter.